As the year winds down, most small business owners are focused on closing deals, hitting targets, and preparing for the next big push. But there’s one critical area that often gets rushed—or worse, ignored—until it’s too late: year-end tax planning.

Done right, it’s not just about compliance. It’s a powerful opportunity to reduce tax liability, improve cash flow, and set your business up for a stronger financial future.

Taxes aren’t just a once-a-year obligation—they’re a year-round strategy. Waiting until filing season means missing out on valuable opportunities to optimize your finances.

Smart year-end planning helps you:

Minimize taxable income legally

Take advantage of available deductions and credits

Avoid last-minute surprises

Gain clarity on your financial position

In short, it gives you control instead of leaving things to chance.

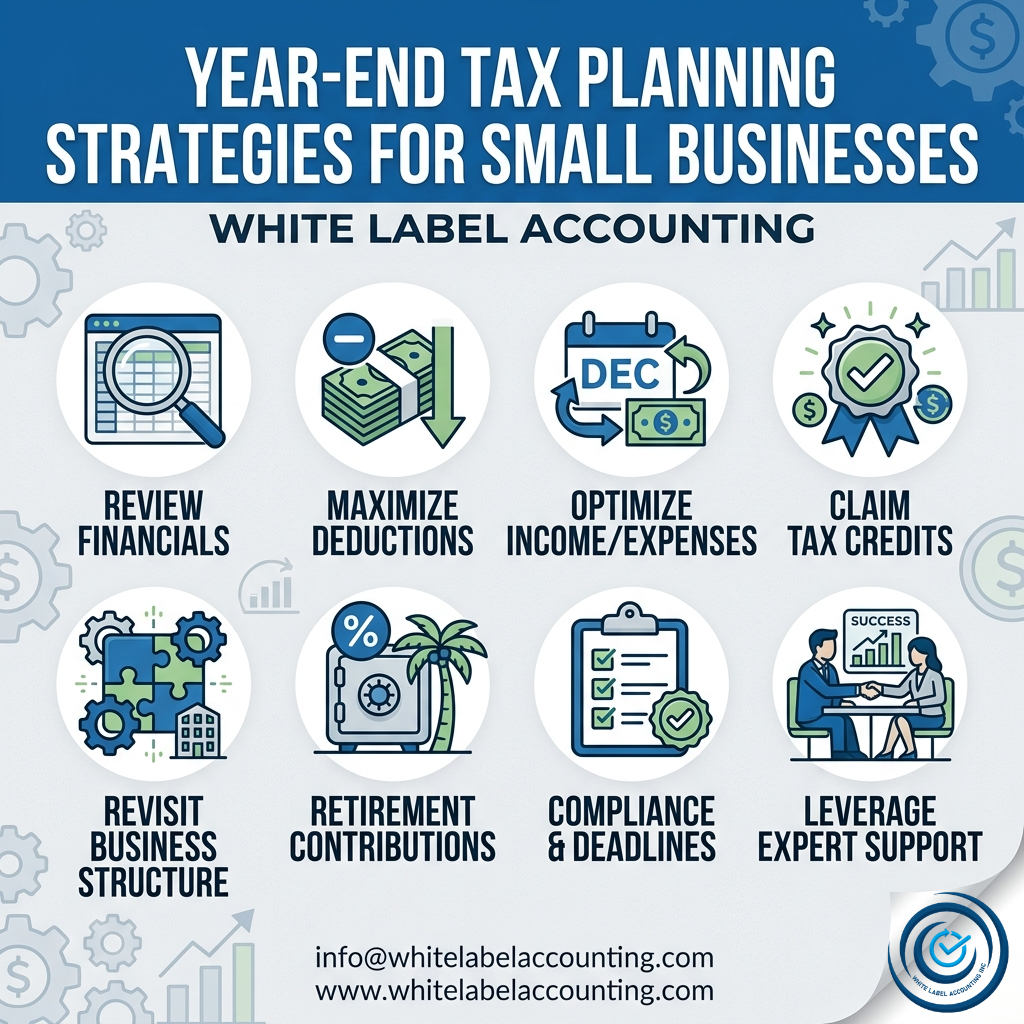

Before making any tax decisions, get a clear picture of where your business stands.

Analyze profit and loss statements

Review cash flow trends

Identify high-expense areas

Spot any inconsistencies or missed entries

Accurate, up-to-date books are the foundation of effective tax planning.

Deductions can significantly lower your taxable income, but timing and relevance matter.

Consider:

Purchasing necessary equipment before year-end

Prepaying certain business expenses (if beneficial)

Writing off bad debts

Claiming home office or vehicle expenses (if applicable)

The goal isn’t just to spend more—it’s to spend smart.

One of the most effective strategies is managing when income and expenses are recognized.

Defer income to the next year (if it makes sense)

Accelerate expenses into the current year

Align revenue recognition with your tax strategy

This approach can help smooth out your tax burden and improve cash positioning.

Unlike deductions, tax credits directly reduce the amount of tax you owe.

Depending on your business, you may qualify for:

Research and development (R&D) credits

Energy efficiency incentives

Hiring or training-related credits

These are often underutilized, so it’s worth exploring what applies to your industry.

Your current structure may not be the most tax-efficient as your business grows.

Sole proprietorship vs. LLC vs. corporation

Potential benefits of S-corp election

Impact on liability and tax rates

A quick review at year-end can uncover opportunities for long-term savings.

Contributing to retirement plans isn’t just good for the future—it can also reduce your taxable income now.

Options may include:

SEP-IRA

Solo 401(k)

Other qualified plans

This strategy allows you to invest in yourself while lowering your tax burden.

Missed deadlines and inaccurate filings can lead to penalties that eat into your profits.

Ensure all records are complete and organized

Verify payroll taxes and filings

Double-check reporting requirements

Staying compliant is just as important as saving money.

Tax laws change frequently, and keeping up can be overwhelming. Partnering with professionals ensures:

Accurate filings

Strategic tax planning

Identification of overlooked opportunities

Peace of mind

Outsourcing your accounting and tax preparation can free up your time while improving financial outcomes.

Year-end tax planning isn’t just a financial task—it’s a strategic advantage. The decisions you make now can have a lasting impact on your business’s profitability and growth.

Instead of scrambling at the last minute, take a proactive approach. With the right planning, you can close the year strong and start the next one even stronger.

Copyright © 2025 White Label Accounting Inc. All Rights Reserved | Developed by WITH U Technology Pvt. Ltd.