Operating a business successfully requires a crystal-clear understanding of financial figures. Yet, many small and micro enterprise owners, startup founders, and beginning accounting practitioners often find themselves looking at a balance discrepancy wondering exactly where the data went wrong.

This guide provides a comprehensive roadmap for mastering the accounting reconciliation process, ensuring your financial statements are accurate, your audit risks remain minimized, and your business stays fully tax-compliant.

At its core, accounting reconciliation is a fundamental financial control process that verifies the consistency across multiple sets of financial records. It is the practice of ensuring that two independent records—such as your business’s ledger and your bank statement—agree with one another.

The records subject to regular reconciliation encompass a wide range of financial documents, including:

General ledgers within automated accounting software

Bank and credit card statements

Corporate loan documents

Payroll records and distributions

State and Federal tax filings

Implementing a structured reconciliation workflow offers three main advantages:

Enhancing Financial Accuracy: Ensures that your internal accounting balance accurately reflects actual real-world capital.

Mitigating Fraud Risk: Consistent cross-checks facilitate the prompt identification of unauthorized withdrawals, altering of checks, or irregular transactions.

Ensuring Compliance: Keeps your records clear for state or federal tax regulations, dropping the risks of unexpected audit corrections.

Ultimately, failure to perform reconciliation consistently over time leads to an accumulation of compounding bookkeeping errors. This makes resolving financial discrepancies a costly, time-consuming nightmare down the road.

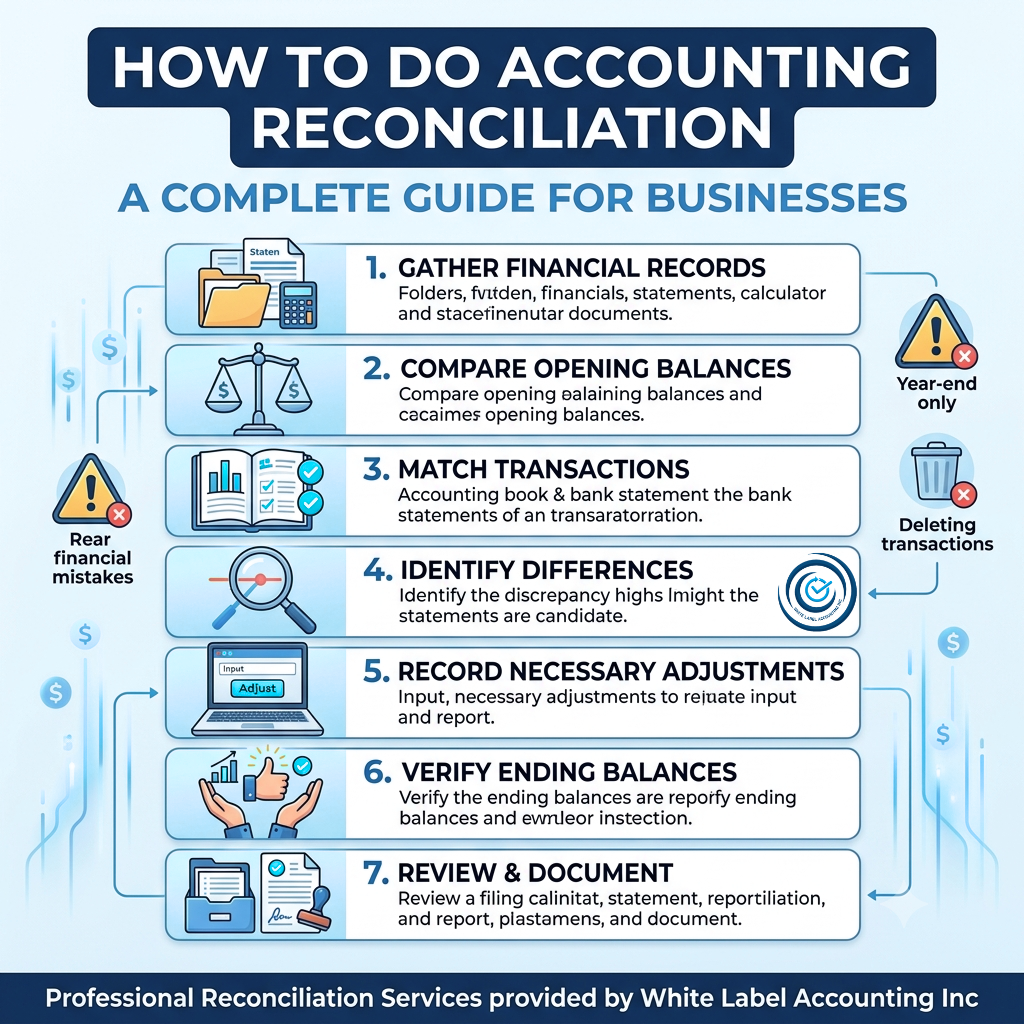

To establish standard procedures within your organization, follow this step-by-step framework to process reconciliations systematically.

Step 1: Gather All Relevant Financial Records

Before running numbers, ensure you have verified the completeness of your specific reconciliation period (e.g., the exact calendar month). Assemble all necessary records:

Bank and credit card statements

Accounting reports (General ledger trial balances)

Physical or digital invoices, receipts, and deposit slips

Confirm that the opening balance figure in your current accounting period exactly matches the closing balance figure from your previous reconciliation period.

Important Rule: Investigate and resolve any discrepancies arising from prior period record inaccuracies or unaddressed adjusting entries before matching new transactions.

Compare your internal ledger entries directly against your external statements. Review every entry type across:

Deposits and electronic fund transfers (EFTs)

Vendor payments and invoice settlements

Bank service charges, transaction fees, and earned interest

Transactions with matching entries across all data sets should be immediately marked as clear.

Isolate items that do not mirror one another. Thoroughly document common industry reconciliation issues such as:

Outstanding Checks: Written checks recorded in books but not yet cashed by the payee.

Deposits in Transit: Cash or checks received and recorded by the business but not yet processed by the bank.

Data Entry Errors: Transposition errors (e.g., typing $450 instead of $540).

Complete a comprehensive analysis of these discrepancies prior to initiating any final balancing steps.

When differences are legitimate—such as monthly bank service fees, interest earnings, or newly discovered unrecorded transactions—you must post adjusting entries to bring your books up to date. All adjustments must be fully supported by original source documentation to remain compliant for future inspection.

To help scale your operations safely, use these cross-industry reference benchmarks to manage frequency and isolate errors:

Not every ledger demands daily inspection. Structuring your calendar saves time while preserving control.

|

Account Type |

Recommended Frequency |

Primary Focus Area |

|

Cash & Operating Banks |

Daily / Weekly |

Cash flow tracking, fraud identification |

|

Credit Cards & Lines of Credit |

Weekly / Monthly |

Expense control, unauthorized charges |

|

Accounts Receivable (A/R) |

Monthly |

Client aging invoices, matching payment receipts |

|

Accounts Payable (A/P) |

Monthly |

Vendor statement validation, preventing double pay |

|

Payroll & Tax Accounts |

Per Pay Period / Quarterly |

Tax allocation match, payroll run validation |

To consider a reconciliation complete, your financial teams must adhere to two golden rules:

Continuous Investigation: If the adjusted book balance does not reconcile perfectly with the statement balance, continuous investigation must be conducted until the exact root cause of the discrepancy is identified. Zero out the difference—never use "plug" numbers.

Document Preservation: A complete set of reconciliation-related documentation must be systematically archived. This supports subsequent third-party audits and retrospective reviews of corporate accounting records.

Micro, Small, and Medium Enterprises (MSMEs) frequently run into structural bottlenecks. Keeping track of seven common reconciliation scenarios and avoiding the six frequent reconciliation errors requires specialized expertise that internal teams may lack.

Without deep technical insight, errors lead to severe financial reporting flaws and legal tax penalties.

Outsourcing this critical task to qualified providers yields measurable structural benefits:

Guaranteed Accuracy: Eradicates data transposition errors.

Advanced Fraud Protection: Neutralizes operational vulnerabilities through external oversight.

Audit Readiness: Preserves clean, organized ledger trails for sudden regulatory inquiries.

Optimized Cash Flow Transparency: Delivers precise metrics on true available capital.

Time Savings: Frees founders to focus on product-market fit and core scaling objectives.

Strategic Decision Support: Powers data-driven choices using pristine balance sheets.

For businesses facing limited professional accounting capacity, White Label Accounting Inc. offers a comprehensive suite of financial management solutions. Their structured portfolio spans seven full-category offerings, putting an emphasis on vital foundational solutions:

Standardized Account Reconciliation: Eliminating rolling accounting variances month-over-month.

Catch-Up Bookkeeping: Correcting months or years of backlogged, unorganized entries to make your business current.

White Label Accounting Inc. utilizes a clear, modular knowledge framework designed to simplify complex financial structures. By delivering clear, practical knowledge first, they establish professional credibility while seamlessly guiding you toward the exact service tier your company needs.

Standardized account reconciliation has consistently served as a fundamental pillar for enterprises to mitigate financial risks and maintain long-term, stable operations. Don't let backlogged ledgers slow down your operational momentum.

Copyright © 2025 White Label Accounting Inc. All Rights Reserved | Developed by WITH U Technology Pvt. Ltd.