Public understanding of accounting is frequently limited to the standardized bookkeeping processes businesses use to track sales, expenses, and profitability. However, accounting for credit unions—which are member-owned financial institutions—requires a level of specialized expertise that extends far beyond standard commercial practices. This divergence is primarily driven by fundamental differences in organizational missions, ownership structures, and regulatory environments.

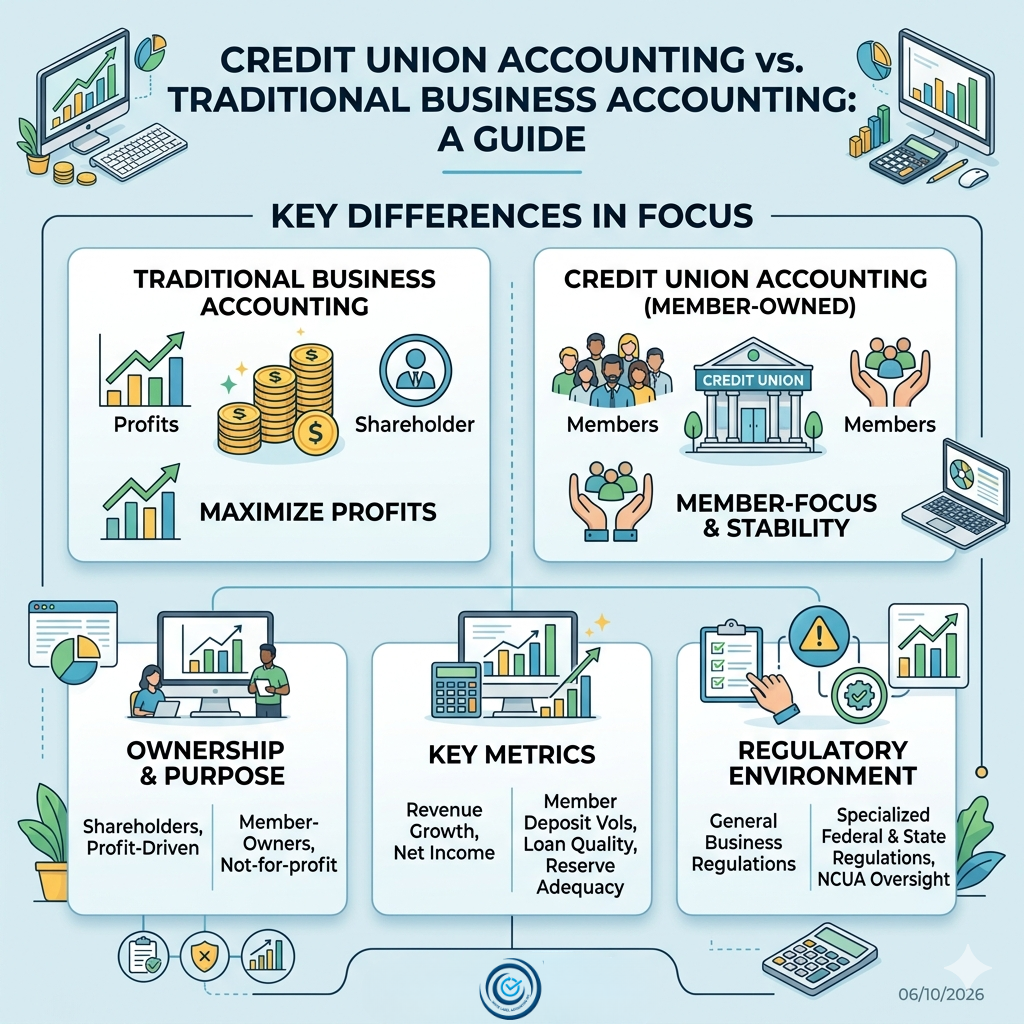

Understanding the difference in Credit Union for accounting

While traditional commercial enterprises prioritize maximizing shareholder wealth through metrics like revenue growth and profit margins, a credit union's primary objective is to provide its members with competitive loan rates, enhanced savings options, and reduced service fees. Consequently, credit union accounting must focus on four critical dimensions: member deposit volumes, loan portfolio quality, regulatory capital requirements, and reserve adequacy.

Reason for accurate Credit union accounting

For credit union leadership, precise accounting data is indispensable for evaluating loan performance, monitoring institutional liquidity, and formulating long-term strategies. Similarly, regulatory agencies rely on standardized financial reports as the primary benchmark for assessing an institution's safety and soundness. Common accounting errors—such as inaccurate loan balances, misclassified deposit accounts, and erroneous loan loss provisions—can precipitate a cascade of operational and compliance risks. Conversely, rigorous accounting practices deliver six essential functions: ensuring regulatory compliance, managing liquidity risk, safeguarding member interests, supporting strategic decision-making, optimizing pricing structures, and mitigating credit losses.

Key Areas for Credit Union Accounting

The following sections will analyze the strategic positioning, reporting criteria, and operational requirements of three primary accounting domains to help industry professionals navigate these specialized standards. Investment accounting, for instance, remains a critical focus during credit union audits and reviews, as these institutions routinely invest their surplus funds in various approved financial instruments. The accounting processes for financial instruments, such as certificates of deposit and government securities, must fulfill three fundamental requirements: precise asset valuation, appropriate revenue recognition, and comprehensive compliance with internal investment policies. Persistent shifts in the interest rate environment over recent years have significantly heightened the strategic importance of this discipline.

Across the industry, credit unions predominantly encounter four primary accounting challenges: continually evolving regulatory reporting mandates, a substantial increase in transaction volumes driven by membership growth, heightened complexity in estimating loan losses due to macroeconomic fluctuations, and the critical necessity to enhance internal controls and reconciliation procedures through the integration of disparate business systems.

While many institutions historically relegated account reconciliation to a routine administrative function, it is a vital component of internal control. Timely and standardized reconciliation ensures the accuracy of cash and investment balances, the completeness of loan records, the alignment of deposit accounts with supporting systems, and the overall integrity of financial reporting. Furthermore, it facilitates the initiative-taking identification of significant operational risks.

Automation technology can optimize efficiency and alleviate administrative burdens by managing five specific functions: transaction matching, bank reconciliation, exception reporting, financial reporting, and data analysis. Nevertheless, technology cannot supplant the critical role of professional accounting personnel in executing reviews, investigating anomalies, and exercising professional judgment. Additionally, automated systems cannot independently adapt to every nuanced business decision or regulatory shift.

Given that most credit unions operate with lean accounting departments amid increasingly intricate regulatory landscapes, professional accounting support is indispensable. This specialized support encompasses seven key areas: monthly bookkeeping, account reconciliation, financial statement preparation, regulatory reporting assistance, accounting remediation projects, internal control evaluations, and year-end accounting support. These services furnish management with the reliable financial intelligence requisite for informed decision-making and align with the rapid evolution of the financial services sector. The authors assert that credit unions presently encounter three primary challenges: escalating competition, shifting regulatory frameworks, and heightened member expectations. Enhancing accounting methodologies enables these institutions to achieve financial stability and foster trust. Beyond mere numerical processing, accounting serves essential strategic functions by protecting assets, facilitating growth, and ensuring long-term viability. By establishing accurate systems, conducting prompt account reconciliations, and instituting professional oversight, credit unions can elevate financial reporting from a basic compliance obligation into a strategic catalyst for institutional advancement.

Copyright © 2025 White Label Accounting Inc. All Rights Reserved | Developed by WITH U Technology Pvt. Ltd.