Running a rental property business or hosting on Airbnb can be incredibly lucrative, but it comes with a unique set of financial headaches. Unlike traditional businesses, real estate tracking requires balancing unpredictable income streams, managing security deposits, and navigating specific tax rules.

Whether you manage long-term leases or flip a vacation property every three days, keeping your books pristine is the difference between a thriving business and a stressful tax season. Here is how to handle your accounting like a pro.

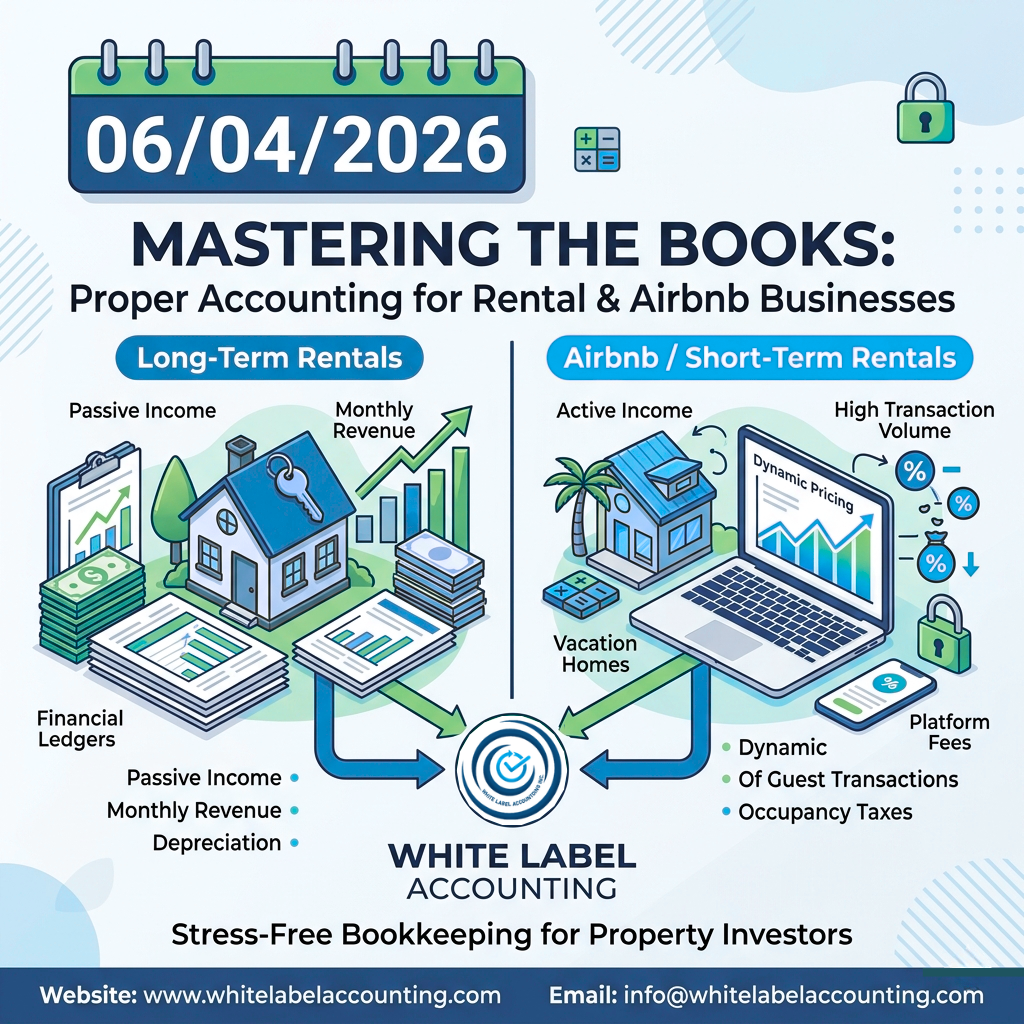

The very first step is understanding that standard rentals and short-term Airbnb stays are treated differently by both accounting standards and tax authorities.

Long-Term Rentals: Generally generate passive income. Your tracking focuses heavily on monthly recurring revenue, standard property maintenance, and long-term depreciation.

Airbnb/Short-Term Rentals: Often classified as active business income if you provide substantial services (like regular cleaning, breakfast, or concierge services). The transaction volume is much higher, and you have to account for platforms fees, dynamic pricing, and occupancy taxes.

To keep your business running smoothly, implement these foundational accounting habits from day one:

Never mix personal expenses with your property expenses. Open a dedicated business bank account and credit card for your rental business. If you own multiple properties, consider tracking them as separate "classes" or "tags" within your accounting software to see exactly which asset is making money and which is costing you.

This is where many property owners make costly mistakes:

Repairs: Fixing a broken window or repairing a leaky pipe. These are current expenses and can be deducted fully in the year they happen.

Improvements (Capital Expenditures): Replacing the entire roof or remodeling a kitchen. These add value to the property and must be capitalized and depreciated over several years.

Airbnb payouts are sent after their host fee (usually 3%) and sometimes local occupancy taxes are deducted.

The Rule: Do not just record the cash hitting your bank account as your gross revenue. You must record the full amount the guest paid as Gross Income, and then record the platform cut as a Merchant/Platform Fee Expense. Failing to do this distorts your true gross income on your tax returns.

To understand if your properties are actually profitable, look beyond your bank balance and monitor these three metrics:

|

Metric |

What It Measures |

Why It Matters |

|

Cash Flow |

Total cash coming in minus cash going out. |

Tells you if you can pay your mortgage and bills this month. |

|

Net Operating Income (NOI) |

All revenue minus necessary operating expenses (excluding mortgage principal). |

Measures the property's ability to generate income independently of its financing. |

|

Cap Rate (Capitalization Rate) |

NOI divided by the current market value of the property. |

Helps you compare the profitability of different real estate investments. |

Manually tracking receipts and mileage in a spreadsheet gets messy fast. Utilizing modern, cloud-based accounting platforms (like QuickBooks Online or Xero) integrated with specialized property management tools (like Hospitable or Guesty for Airbnb) allows you to automate invoice generation, expense categorization, and bank reconciliations.

Keeping up with real estate tax laws, cleaning fees, and platform payouts can quickly feel like a full-time job on top of your actual hosting duties.

If you want to ensure your rental or Airbnb books are audit-proof and optimized for maximum tax deductions, let the professionals handle it.

Reach out to White Label Accounting today for tailored, stress-free bookkeeping designed specifically for property investors and short-term rental hosts!

Copyright © 2025 White Label Accounting Inc. All Rights Reserved | Developed by WITH U Technology Pvt. Ltd.