In the world of business, bookkeeping is often treated as a background task—something to “handle later.” But small errors in your books can quietly snowball into serious financial issues. From cash flow confusion to compliance risks, bookkeeping mistakes can cost more than just money—they can cost opportunities.

The good news? Most of these mistakes are preventable. Let’s explore the most common bookkeeping pitfalls and how modern businesses can avoid them with smarter systems and strategies.

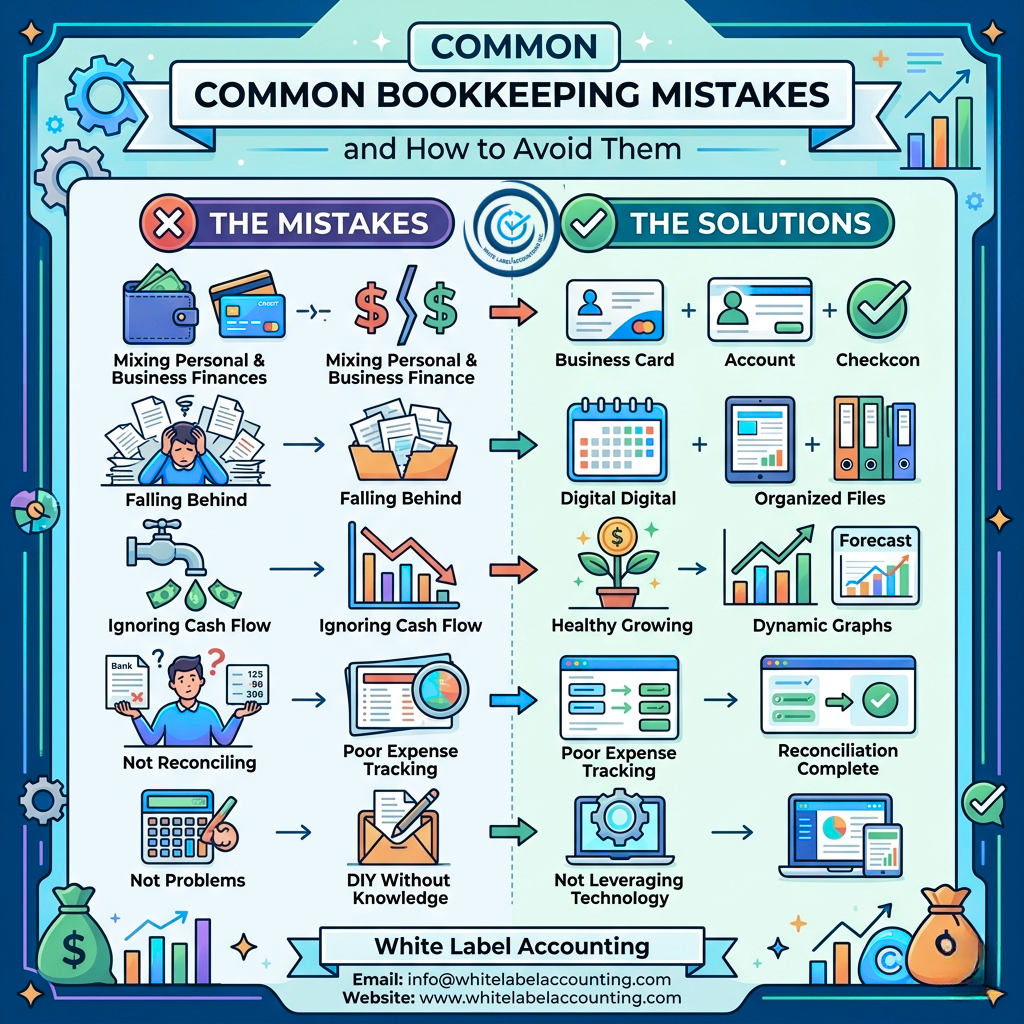

One of the most frequent mistakes entrepreneurs make is blending personal and business transactions. It may seem harmless at first, but it quickly leads to confusion, inaccurate reporting, and tax complications.

How to avoid it:

Open a dedicated business bank account and use it exclusively for company transactions. This simple step creates clarity and ensures your financial records remain clean and professional.

Delaying bookkeeping is like ignoring a slow leak—it only gets worse over time. When records pile up, errors become harder to track, and financial visibility disappears.

How to avoid it:

Adopt a consistent schedule—weekly or monthly—to update your books. Better yet, use cloud-based tools or outsource to professionals to ensure your records are always current.

Untracked or misclassified expenses can distort your financial reports and lead to missed tax deductions. Over time, this impacts profitability analysis and budgeting accuracy.

How to avoid it:

Use digital tools to capture receipts and categorize expenses in real time. Consistent labeling helps you understand spending patterns and maximize deductions.

Profit doesn’t always equal cash in hand. Many businesses fail because they don’t monitor their cash flow closely enough.

How to avoid it:

Track incoming and outgoing cash regularly. Create cash flow forecasts to anticipate shortages and plan ahead. Staying proactive helps you avoid unexpected financial stress.

Skipping bank and credit card reconciliations can leave discrepancies unnoticed. Over time, these small mismatches can lead to major inaccuracies.

How to avoid it:

Reconcile accounts at least once a month. This ensures your records match actual transactions and helps catch errors early.

While handling bookkeeping yourself can save money initially, lack of expertise often leads to costly mistakes—especially as your business grows.

How to avoid it:

Invest in professional support or training. Outsourced bookkeeping services provide expertise, accuracy, and scalability without the overhead of an in-house team.

Many businesses generate financial reports but rarely analyze them. Without reviewing these insights, you’re missing opportunities to improve performance.

How to avoid it:

Regularly review key reports like profit & loss statements, balance sheets, and cash flow statements. Use these insights to guide your business decisions and strategy.

Waiting until tax season to organize finances can lead to stress, errors, and penalties.

How to avoid it:

Maintain organized records throughout the year and set aside funds for tax obligations. Proactive tax planning ensures compliance and avoids last-minute surprises.

Relying on manual processes increases the risk of human error and inefficiency.

How to avoid it:

Adopt modern accounting software that automates tasks like invoicing, expense tracking, and reporting. Automation saves time and improves accuracy.

As your business grows, outdated bookkeeping systems can’t keep up, leading to inefficiencies and data gaps.

How to avoid it:

Choose scalable solutions that grow with your business. Outsourcing or upgrading your systems ensures you’re always prepared for expansion.

Bookkeeping mistakes are common—but they don’t have to be inevitable. By building disciplined habits, leveraging technology, and seeking expert support, businesses can turn bookkeeping into a strength rather than a struggle.

Accurate financial records aren’t just about compliance—they’re about clarity, confidence, and control. When your books are in order, your business is better positioned to grow, adapt, and succeed in an ever-changing market.

Copyright © 2025 White Label Accounting Inc. All Rights Reserved | Developed by WITH U Technology Pvt. Ltd.