Bookkeeping is the foundation of every successful business. Accurate financial records help organizations make informed decisions, maintain compliance, and monitor overall financial health. However, even small bookkeeping mistakes can lead to serious problems such as cash flow issues, incorrect tax filings, or poor financial planning.

Many businesses—especially startups and growing companies—struggle with maintaining precise financial records due to time constraints, lack of expertise, or outdated systems. Understanding common bookkeeping mistakes and learning how to avoid them can help businesses maintain accuracy and financial stability.

Below are some of the most frequent bookkeeping errors and practical strategies to prevent them.

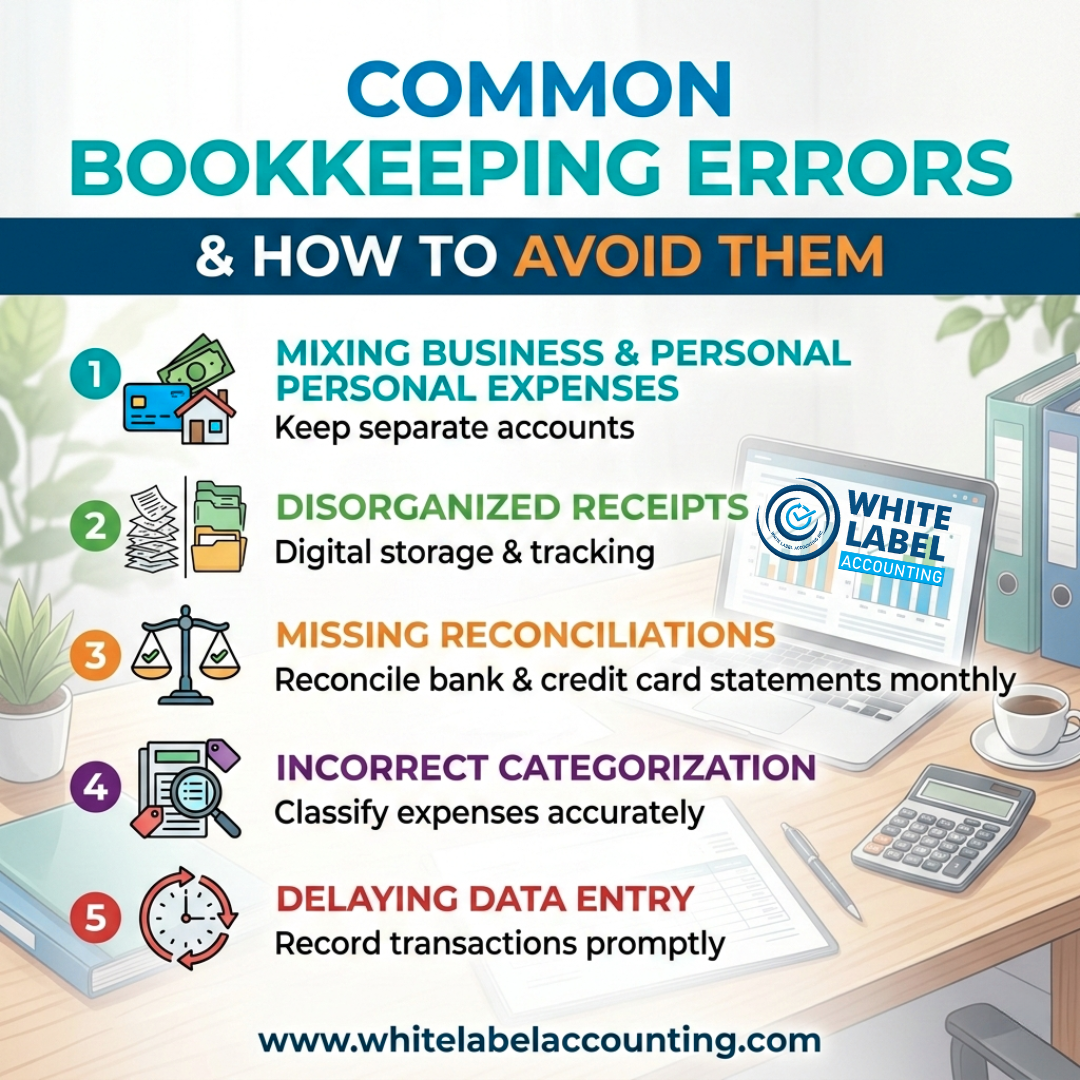

One of the most common mistakes small business owners make is combining personal and business transactions in the same bank account. This practice can make bookkeeping confusing and create complications during tax season.

How to Avoid It

Open a dedicated business bank account and credit card for all company transactions. Keeping financial activities separate simplifies record-keeping, improves financial clarity, and ensures smoother audits and tax filings.

When bookkeeping is postponed for weeks or months, it becomes much harder to track transactions accurately. Missing receipts, forgotten expenses, and delayed entries can quickly lead to incomplete financial records.

How to Avoid It

Adopt a consistent bookkeeping routine. Recording transactions weekly—or even daily for high-volume businesses—ensures that financial data remains accurate and up to date.

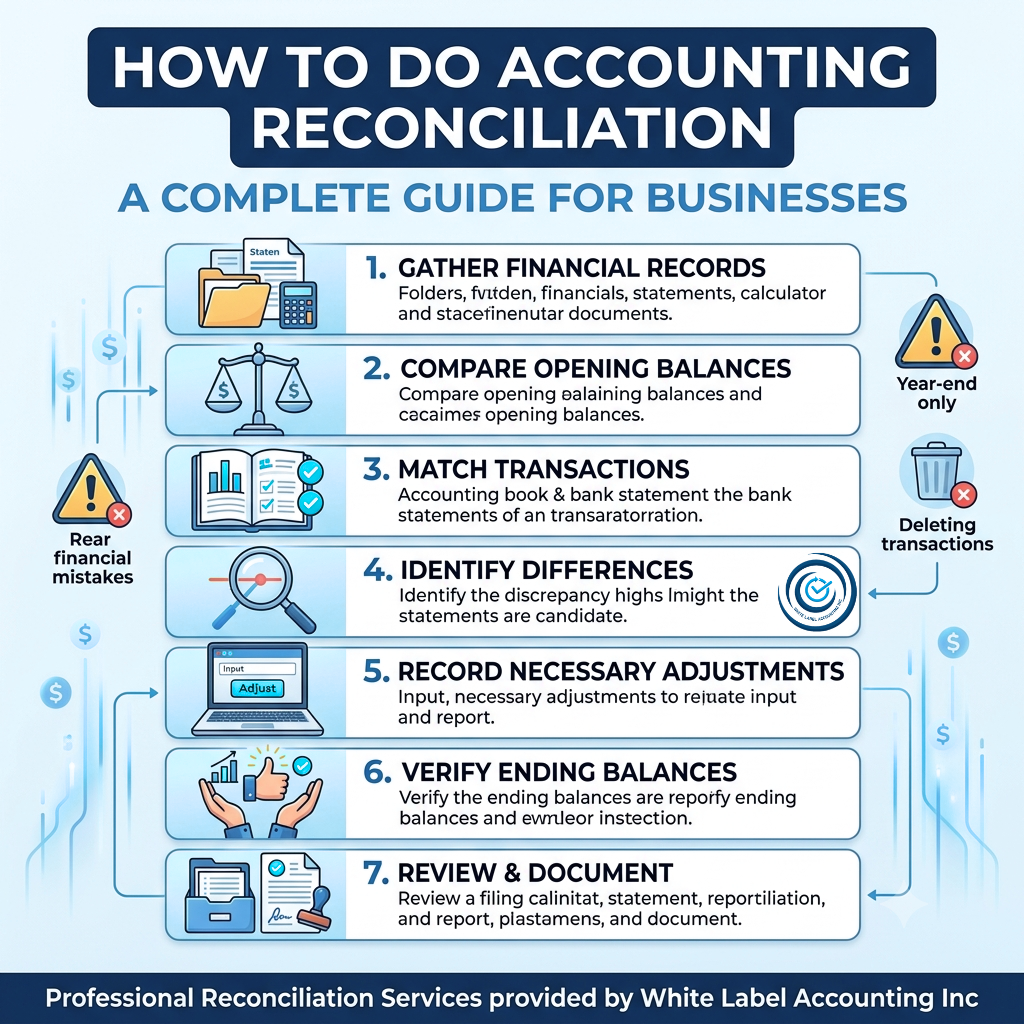

Reconciliation is the process of comparing internal financial records with bank statements to ensure everything matches. Skipping this step can allow unnoticed discrepancies to grow over time.

How to Avoid It

Perform bank and credit card reconciliations at least once a month. This helps identify missing entries, duplicates, or unauthorized transactions early.

Misclassifying expenses is a surprisingly common issue. Placing transactions under the wrong category can distort financial reports and affect tax deductions.

How to Avoid It

Create a clear chart of accounts and follow consistent categorization rules. Accounting software can also help automate expense classification and reduce errors.

Receipts and financial documentation serve as proof of transactions. Losing them can make it difficult to justify expenses during tax filing or financial audits.

How to Avoid It

Digitize receipts and store them in secure cloud-based systems. Many bookkeeping tools allow users to attach receipts directly to transactions for easy access later.

Small purchases might seem insignificant, but over time they can accumulate and create discrepancies in financial records.

How to Avoid It

Record every transaction—no matter how small. Maintaining complete financial data ensures more accurate reporting and budgeting.

Many businesses initially manage bookkeeping internally to save money. However, lack of professional knowledge can lead to errors that cost far more to fix later.

How to Avoid It

Consider working with experienced bookkeeping professionals or outsourcing services. Expert support ensures compliance, accuracy, and efficiency in financial management.

Bookkeeping isn't just about recording numbers—it’s also about understanding them. Businesses that fail to review financial reports regularly may miss warning signs such as declining profits or rising expenses.

How to Avoid It

Review financial statements such as profit and loss reports, balance sheets, and cash flow statements on a monthly basis. These insights help guide better business decisions.

Accurate bookkeeping plays a critical role in business growth. By avoiding common errors and implementing structured financial processes, companies can improve financial visibility and reduce operational risks.

Many organizations choose professional accounting partners to handle bookkeeping tasks efficiently. Expert services provide structured systems, advanced tools, and experienced professionals who ensure financial records remain accurate and compliant.

At White Label Accounting, businesses and accounting firms can access reliable bookkeeping support that enhances efficiency, accuracy, and financial transparency.

Copyright © 2025 White Label Accounting Inc. All Rights Reserved | Developed by WITH U Technology Pvt. Ltd.